Lets explore the importance of your credit score in the mortgage application process and how it can impact your eligibility for a loan

Table of Contents:

- What is a Credit Score?

- Why Does Your Credit Score Matter?

- How is Your Credit Score Calculated?

- Key Factors Affecting Your Credit Score

- Understanding Credit Score Ranges

- Checking Your Credit Score FREE

- Improving Your Credit Score

- How to Dispute Inaccuracy

- Conclusion

- Search Homes for Sale

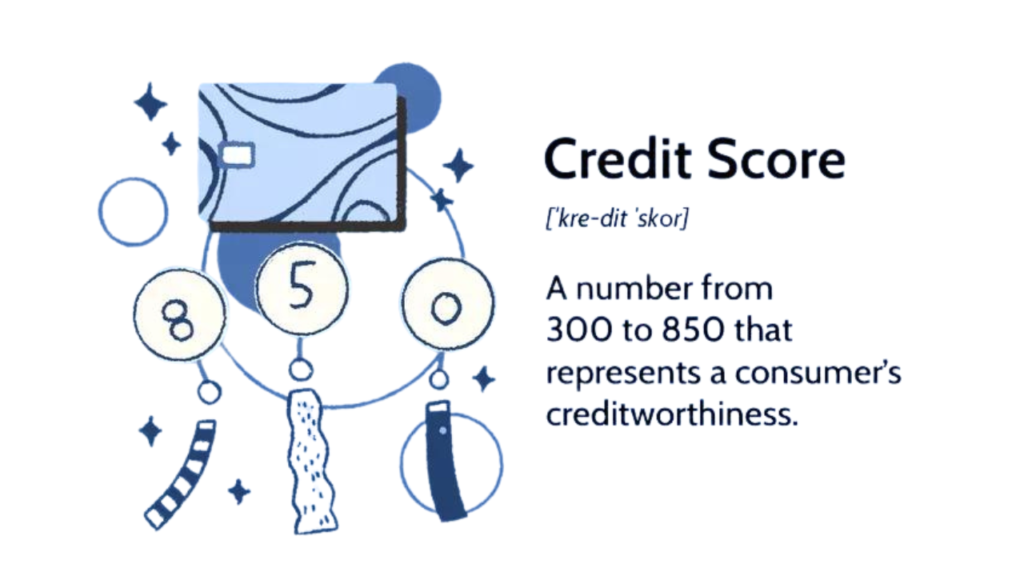

What is a Credit Score?

Your credit score is a numerical representation of your creditworthiness.

It’s based on various factors such as your payment history, amounts owed, length of credit history, new credit accounts, and types of credit used

Why Does Your Credit Score Matter?

Lenders use your credit score to assess the risk of lending you money.

A higher credit score indicates lower risk, making you more likely to qualify for a mortgage and secure favorable terms such as lower interest rates and higher loan amounts.

How is Your Credit Score Calculated?

Credit scores are typically calculated by credit reporting agencies such as Experian, Equifax, and TransUnion.

They use complex algorithms to analyze your credit history and assign you a score ranging from 300 to

850.

Key Factors Affecting Your Credit Score:

- Payment History: Your track record of making on-time payments.

- Credit Utilization: The amount of credit you’re using compared to your total available credit

- Length of Credit History: How long you’ve had credit accounts open.

- Types of Credit: The variety of credit accounts you have, such as credit cards, loans, and mortgages.

- New Credit: How often you apply for and open new credit accounts.

Understanding Credit Score Ranges:

- Excellent (800-850): You’re likely to qualify for the best mortgage rates and terms.

- Good (670-799): You’re considered a reliable borrower, but rates may not be as favorable as those with excellent credit.

- Fair (580-669): You may face challenges in qualifying for a mortgage, and rates may be higher.

- Poor (300-579): It may be difficult to qualify for a mortgage, and you may need to work on improving your credit before applying.

Checking Your Credit Score:

It’s essential to regularly monitor your credit score to identify any inaccuracies or issues that could affect your mortgage eligibility.

According to federal law, consumers are entitled to one free annual credit report from each major credit reporting agency.

You can request your free credit report from each of the three major credit bureaus once every year through

AnnualCreditReport.com

or by calling 1-877-322-8228.

Improving Your Credit Score:

If your credit score isn’t where you want it to be, there are steps you can take to improve it:

- Make all payments on time.

- Pay down existing debt to lower your credit utilization ratio.

- Avoid opening new credit accounts unless necessary.

- Regularly check your credit report for errors and dispute any inaccuracies.

How to Dispute Inaccuracy?

- Get a copy of your credit report.

- Contact the credit bureau(s) that have the mistake.

- Explain the error in writing.

- Include any supporting documents.

- Submit your dispute.

Conclusion:

Your credit score plays a significant role in determining your mortgage eligibility and the terms you’ll be offered.

By understanding how your credit score is calculated and taking steps to improve it, you can increase your chances of securing a mortgage that meets your needs.