Mortgage pre-approval is a lender’s formal, verified estimate of how much you can borrow, based on a hard credit pull and reviewed financial documents. It differs from prequalification, which is a quick, unverified estimate that carries little weight in a competitive offer. Knowing how to get a mortgage pre approval fast matters most in markets like Orlando, Daytona Beach, and Melbourne, FL, where homes in Meadow Woods, Hunters Creek, and Southchase move quickly. A verified pre-approval letter tells sellers you are a serious buyer, not just someone browsing. The faster you secure it, the better your position when the right home hits the market.

What documents do you need for a fast mortgage pre-approval?

Your document package is the single biggest factor in how fast you get approved. Lenders cannot move forward without verified financial information, and any missing item stops the clock.

The five core document categories every borrower needs are:

- W-2 forms from the last two years

- Federal tax returns from the last two years

- Pay stubs from the last 30 days

- Bank statements from the last 2–3 months

- Government-issued photo ID

Missing any core documents is the top reason a 24-hour turnaround stretches into a week or longer. That one missing bank statement can put you at the back of the line.

Self-employed borrowers face a longer road. Self-employed applicants typically need business financial statements, profit and loss reports, and additional tax schedules on top of the standard package. If that describes you, start gathering those documents at least two weeks before you plan to apply.

| Document | Why it matters |

|---|---|

| W-2s (last 2 years) | Confirms employment history and income stability |

| Tax returns (last 2 years) | Verifies reported income, especially for self-employed buyers |

| Pay stubs (last 30 days) | Shows current income and pay frequency |

| Bank statements (2–3 months) | Proves available funds for down payment and reserves |

| Photo ID | Confirms identity for underwriting compliance |

Pro Tip: Scan and save every document as a clearly labeled PDF before you apply. Name files like “2024_W2_Smith” so your loan officer can find them instantly. Organized uploads speed up the review process significantly.

How to choose the right lender and pre-approval method for speed

Not all lenders move at the same pace, and the method you choose directly affects how fast you get your letter.

The first distinction to understand is prequalification versus pre-approval. Prequalification is an instant, soft-credit estimate. Pre-approval involves a hard credit pull and full document review. Digital pre-approval processes may provide instant results, but they are often conditional and not final until full underwriting is complete. A fully verified pre-approval letter carries far more weight when you make an offer.

When evaluating lenders, look for these speed indicators:

- Automated underwriting systems: These process applications faster than manual review, often within hours.

- Same-day conditional approval programs: Some lenders offer programs where a well-prepared borrower can receive an approval within one business day.

- Dedicated loan officers: A single point of contact who responds quickly reduces back-and-forth delays.

- Digital document portals: Uploading directly to a secure portal is faster than emailing attachments.

Lenders offering same-day approvals require borrowers to submit all documents within very tight timeframes, sometimes as short as eight business hours. Missing those deadlines usually disqualifies you from the fast-track program entirely.

Pro Tip: Call the lender before you apply and ask directly: “What is your average pre-approval turnaround time?” A lender who cannot answer that question clearly is not optimized for speed.

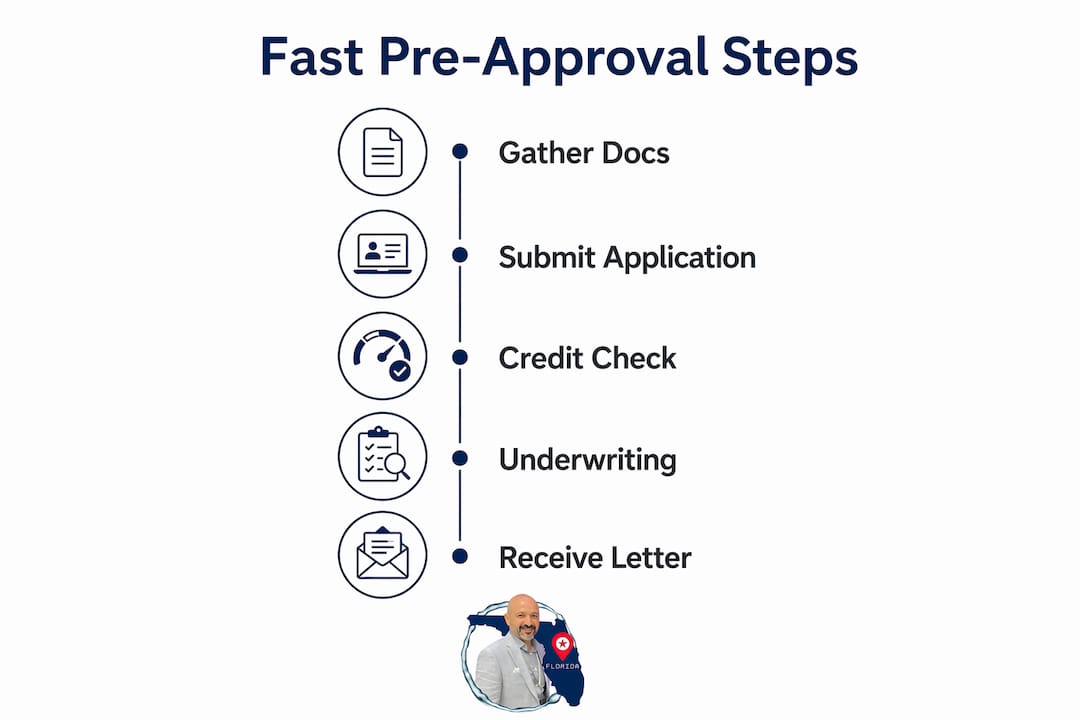

What is the step-by-step process to get pre-approved quickly?

A fast mortgage approval process follows a clear sequence. Skipping or rushing any step creates delays later.

Complete the lender application. Fill out the full application with accurate personal, employment, and financial information. Errors here trigger follow-up requests that add days to your timeline.

Upload all required documents promptly. Submit your complete document package at the same time as your application. Partial submissions are the most common cause of delays. Borrower responsiveness is the linchpin of fast mortgage approvals. Technology only expedites what you enable.

Respond to lender requests the same day. Your loan officer will likely ask follow-up questions or request additional documents. Treat every request as urgent. A 24-hour delay on your end can push your approval back by two or three business days.

Understand the underwriting timeline. Automated underwriting systems can return a decision within hours. Manual underwriting takes longer, sometimes two to five business days. Ask your lender upfront which process they use.

Receive and use your pre-approval letter. Once issued, your letter is typically valid for 60 to 90 days before it requires updating. Use that window to make offers with confidence.

Pro Tip: Set your phone notifications to “on” during the pre-approval process. Loan officers often work on tight schedules. A missed call or a delayed email reply can cost you a full business day.

Your credit score and mortgage eligibility also play a direct role in how smoothly underwriting goes. A strong credit profile reduces the number of conditions a lender attaches to your approval.

What common mistakes delay mortgage pre-approval?

Most delays in the fast mortgage approval process come from borrower errors, not lender slowdowns. Knowing what to avoid is just as important as knowing what to do.

- Submitting incomplete documents. A missing page from a bank statement or a tax return without all schedules attached triggers an immediate request for resubmission.

- Applying with unresolved credit issues. Paying down revolving debt and avoiding new credit inquiries before applying improves your approval odds and reduces conditions.

- Changing your financial situation mid-process. Opening a new credit card, financing a car, or switching jobs while your application is under review can void your approval entirely.

- Confusing prequalification with pre-approval. Some lenders market “instant pre-approval” that is actually a soft credit check generating a conditional offer. True pre-approval requires a full credit pull and underwriting review.

- Ignoring lender follow-up requests. Slow responses are the most controllable delay. Every hour you wait to reply is an hour added to your timeline.

“Pre-approval is a commitment to be audit-ready, not just a formality. Borrowers who treat it that way get their letters fast. Borrowers who treat it casually wait weeks.”

Pro Tip: Before you apply, pull your own credit report at AnnualCreditReport.com and dispute any errors. Inaccurate negative items can trigger underwriting conditions that add days to your approval.

Key Takeaways

Getting a quick mortgage pre-approval requires complete documents, a responsive borrower, and a lender with verified underwriting, not just an instant online estimate.

| Point | Details |

|---|---|

| Documents drive speed | Have W-2s, tax returns, pay stubs, bank statements, and photo ID ready before you apply. |

| Pre-approval beats prequalification | Only a hard credit pull with verified documents produces a letter strong enough for competitive offers. |

| Borrower responsiveness is critical | Responding to lender requests the same day is the fastest thing you can do to speed up approval. |

| Pre-approval letters expire | Most letters are valid for 60–90 days, so time your application close to your home search. |

| Avoid financial changes mid-process | New debt or a job change during underwriting can void your approval and restart the clock. |

What I have seen slow buyers down in Orlando and why it matters

After working with buyers across Meadow Woods, Hunters Creek, Southchase, and BVL, I can tell you the number one reason buyers lose homes is not price. It is preparation. A seller in this market will almost always choose a buyer with a verified pre-approval letter over one with a prequalification printout, even if the prequalified offer is higher.

The buyers I see move fastest are the ones who treat document gathering like a job. They have a folder ready, they respond to their loan officer within the hour, and they understand that the lender’s clock does not pause for the weekend. The buyers who struggle are the ones who apply first and then scramble to find their tax returns.

One thing I tell every first-time buyer I work with: get your pre-approval before you fall in love with a house. Once you find the right home in a neighborhood like Hunters Creek or Southchase, you will not have time to gather documents. The listing will be gone. Your pre-approval letter is your ticket to compete, and getting it fast is entirely within your control.

— Ramy

Ready to buy in Central Florida? Meetramy can help

Buying a home in the Orlando metro area moves fast, and you need a team that moves faster. Meetramy serves buyers across Meadow Woods, Hunters Creek, Southchase, BVL, and surrounding communities with hands-on guidance from the first conversation to closing day.

The Meetramy knowledge hub covers everything from mortgage preparation to down payment requirements, written specifically for buyers in this market. Whether you are a first-time buyer or refinancing your current home, Ramy G Girgis gives you the real-world advice you need to move with confidence. Reach out today and get matched with the right resources for your situation.

FAQ

What is the difference between pre-approval and prequalification?

Pre-approval involves a hard credit pull and verified document review, making it a formal lender commitment. Prequalification is an unverified estimate based on self-reported information and carries little weight in competitive offers.

How fast can I get a mortgage pre-approval?

A well-prepared borrower who submits all documents at once can receive a conditional approval within one business day under same-day mortgage programs. Manual underwriting typically takes two to five business days.

How long is a mortgage pre-approval letter valid?

Most pre-approval letters are valid for 60–90 days. After that, lenders require updated financial documents and a refreshed credit review before reissuing the letter.

What hurts my chances of a quick pre-approval?

Incomplete documents, unresolved credit issues, new debt opened during the application, and slow responses to lender requests are the most common causes of delays.

Do I need a pre-approval letter to make an offer in Florida?

You are not legally required to have one, but sellers in competitive markets like Orlando, Daytona Beach, and Melbourne strongly prefer buyers who present a verified pre-approval letter with their offer.