Mortgage pre-approval is a formal lender evaluation that confirms how much you can borrow before you make an offer on a home. For buyers in South Orlando neighborhoods like Meadow Woods, Hunters Creek, and Southchase, knowing how to get a mortgage pre approval gives you a real edge in a competitive market. The process involves a hard credit pull and underwriting, making it far more credible than a simple pre-qualification. Sellers and agents take pre-approval seriously because it signals genuine buying power. Get this step right, and you walk into every showing with confidence.

How to get a mortgage pre approval: what you need to prepare

Preparation is the single biggest factor in how fast and smoothly your pre-approval goes. Lenders need to verify your identity, income, assets, and debts before they commit to any number. Walking in unprepared adds days or weeks to the process.

The five core document categories every lender requires are:

- Valid government-issued ID: A driver’s license or passport confirms your identity and matches your application.

- Recent pay stubs: Typically the last 30 days. These show your current income level.

- W-2s or tax returns for the past two years: Lenders use these to verify income consistency over time.

- Bank and investment account statements: Usually the last 2–3 months. These confirm your assets and down payment funds.

- Liability disclosures: A full list of current debts, including car loans, student loans, and credit card balances.

Each document answers a specific underwriting question. Pay stubs prove current earnings. Tax returns reveal whether your income is stable or erratic. Bank statements show you have enough saved for a down payment and closing costs. Debt disclosures feed directly into your Debt-to-Income ratio calculation, which lenders weigh heavily.

| Document | Why lenders need it |

|---|---|

| Government-issued ID | Confirms identity and matches application records |

| Recent pay stubs | Verifies current income level |

| W-2s or tax returns (2 years) | Shows income stability over time |

| Bank and investment statements | Confirms assets and down payment availability |

| Liability list | Calculates Debt-to-Income ratio |

Your credit score is equally critical. Conventional lenders typically require a minimum score of 620, while FHA loans may accept scores as low as 500 with a 10% down payment. Check your score before you apply. If it sits below 620, spend 60–90 days paying down revolving balances and disputing any errors on your credit report. You can learn more about how your score affects your options at credit score and mortgage eligibility.

Pro Tip: Stop applying for new credit cards, car loans, or any other credit accounts at least 90 days before you apply for pre-approval. Each hard inquiry chips away at your score.

Step-by-step process to get pre-approved in South Orlando

Getting pre-approved follows a clear sequence. Skipping steps or rushing through them creates delays.

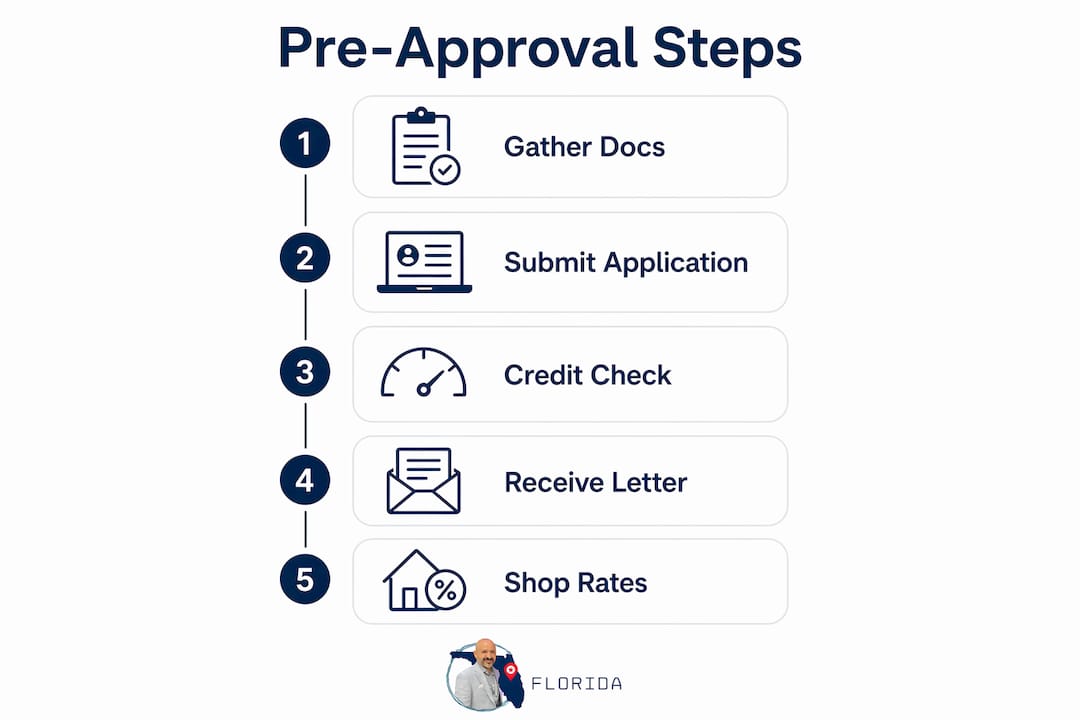

Choose your lender. Compare at least two or three lenders on interest rates, loan types (conventional, FHA, VA, USDA), and customer service responsiveness. Local lenders familiar with the South Orlando market can sometimes move faster on appraisals and title work.

Submit your application. Most lenders offer online portals, in-person appointments, or phone applications. Online portals are fastest for straightforward profiles. Bring all your documents from the checklist above so the lender can review everything in one pass.

Authorize the hard credit pull. The lender will run a hard inquiry on your credit report. This is standard and necessary. It temporarily lowers your score by a few points, but the impact is minor compared to the benefit of having a verified pre-approval letter.

Lender underwrites your file. The underwriter reviews your income, assets, debts, and credit history together. Lenders prioritize financial stability and a manageable Debt-to-Income ratio over raw income numbers alone. A buyer earning $60,000 with minimal debt often qualifies more easily than a buyer earning $90,000 with heavy obligations.

Receive your pre-approval letter. The letter states the loan amount you qualify for, the loan type, and the expiration date. Most letters are valid for 60–90 days.

Timing matters. Simple profiles can receive pre-approval in one business day. Complex cases, including self-employed buyers or those with fluctuating income, can take a week or longer. Self-employment requires two years of business tax returns, profit and loss statements, and sometimes a CPA letter confirming your business is active. Plan accordingly if your income does not come from a traditional W-2 employer.

Pro Tip: Apply with one lender first to get your pre-approval letter, then shop rates with one or two others within a 14-day window. Credit bureaus typically count multiple mortgage inquiries within that window as a single inquiry, protecting your score.

The pre-approval is conditional, not final. It can be rescinded if the home appraisal comes in low or if your financial situation changes before closing. Treat it as a strong starting point, not a guarantee.

What mistakes can derail your mortgage pre-approval?

Most pre-approval problems are self-inflicted. Buyers make financial moves that look routine but send red flags to underwriters.

- Opening new credit accounts: A new car loan or credit card between pre-approval and closing raises your Debt-to-Income ratio and can trigger a denial. Avoid new credit applications until after you close.

- Making large purchases: Buying furniture, appliances, or a vehicle on credit before closing changes your debt profile. Lenders re-verify your credit right before closing.

- Undisclosed debts: Hiding a personal loan or co-signing someone else’s debt creates inconsistencies in your file. Lenders find these during underwriting, and the discrepancy damages your credibility.

- Inconsistent bank deposits: Lenders review bank statements for unusual activity, including gambling transactions, buy-now-pay-later accounts, or large unexplained deposits. Any of these can delay approval or trigger a denial.

- Job changes: Switching employers during the process, especially to a different industry or from salaried to self-employed, resets the income verification clock.

“Pre-approval is conditional and depends on property appraisal and unchanged financial status until closing. Major purchases or changes can negate approval entirely.”

The fix for all of these is the same: stay financially still from the moment you apply until the day you close. Pay your bills on time, keep your spending normal, and communicate any changes to your lender immediately. Transparency with your lender is always better than surprises at closing. For a deeper look at the most common first-time buyer errors in Florida, Ramy Girgis has a dedicated resource worth reading.

Pro Tip: If you receive a large cash gift for your down payment, document it with a signed gift letter from the donor. Lenders require this to confirm the funds are not a loan.

How to use your pre-approval letter effectively in South Orlando

A pre-approval letter is more than a formality. It shows sellers your financial readiness and borrowing capacity before you sign a contract. In South Orlando’s active market, sellers routinely receive multiple offers. An offer backed by a pre-approval letter stands apart from one that is not.

Here is how to use it well:

- Set your real budget. Your pre-approval amount is the ceiling, not the target. Factor in property taxes, HOA fees common in communities like Meadow Woods and BVL, homeowner’s insurance, and maintenance costs when deciding your actual purchase price.

- Move fast on offers. Pre-approval letters typically expire in 60–90 days. If you find the right home within that window, you can make an offer immediately without waiting for financing confirmation.

- Understand the difference between pre-approval and final approval. Pre-approval confirms your financial profile. Final approval also requires a satisfactory property appraisal and a clear title search. Do not skip the home inspection assuming the lender’s appraisal covers everything.

- Renew if needed. If your letter expires before you find a home, contact your lender to renew. Renewal usually requires updated pay stubs and bank statements but does not restart the full process.

Understanding the difference between pre-qualification and pre-approval also helps you communicate clearly with sellers’ agents, who will ask which one you have.

Key Takeaways

Getting pre-approved for a mortgage requires complete documentation, a credit score of at least 620 for conventional loans, and financial stability from application through closing.

| Point | Details |

|---|---|

| Prepare documents first | Gather ID, pay stubs, W-2s, bank statements, and debt disclosures before applying. |

| Credit score threshold | Conventional loans require a minimum 620 score; FHA loans may accept 500 with 10% down. |

| Timeline varies | Simple profiles close in one business day; complex cases like self-employment take a week or more. |

| Stay financially still | Avoid new credit, large purchases, or job changes from application through closing. |

| Pre-approval is conditional | Final approval also depends on property appraisal and unchanged financial status. |

What I’ve learned watching South Orlando buyers win and lose on pre-approval

I’ve worked with buyers across Meadow Woods, Hunters Creek, Southchase, and BVL long enough to see the same patterns repeat. The buyers who get into contract fast are almost always the ones who got pre-approved before they started touring homes. Not during. Before.

The buyers who struggle are usually the ones who fell in love with a home first and then scrambled to get financing. In a market where good homes in the $300,000–$400,000 range move in days, that sequence is backwards. By the time their pre-approval came through, the home was gone.

One thing I tell every buyer I work with: your pre-approval letter is your credibility document. Sellers in South Orlando are not just evaluating your offer price. They are evaluating your ability to close. A clean pre-approval letter from a reputable lender tells them you are serious and ready.

The other thing I see trip people up is the period between pre-approval and closing. Buyers celebrate getting pre-approved and then go buy a car or open a store credit card. That single decision has killed more deals than I care to count. Lenders pull your credit again right before closing. Any new debt shows up, and the numbers change.

My honest advice: treat the pre-approval letter like the starting gun, not the finish line. Stay disciplined, respond to your lender quickly, and keep your finances exactly as they were when you applied.

— Ramy Girgis

Working with Ramy Girgis on your South Orlando home purchase

Hey there! If you are ready to buy a home in Meadow Woods, Hunters Creek, Southchase, or BVL, getting pre-approved is the right first move. Ramy Girgis works with buyers across South Orlando every day and can connect you with trusted local lenders who know this market.

From understanding your financing options to making a strong offer, Ramy Girgis guides you through every step. Visit the homebuyer knowledge hub for guides on down payment requirements, credit scores, and what to expect at closing. When you are ready to talk, reach out directly. The right home is out there, and the right preparation gets you there first.

FAQ

What is the minimum credit score for mortgage pre-approval?

Most conventional lenders require a minimum credit score of 620 for pre-approval. FHA loans may accept scores as low as 500 with a 10% down payment.

How long does mortgage pre-approval take?

Pre-approval typically takes one business day for straightforward financial profiles. Complex cases, such as self-employed buyers, can take a week or longer.

How long is a mortgage pre-approval letter valid?

Most pre-approval letters are valid for 60–90 days. If the letter expires before you find a home, contact your lender to renew it with updated financial documents.

What is the difference between pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on self-reported information. Pre-approval involves a hard credit pull and full document review, making it a much stronger indicator of buying power.

Can my pre-approval be taken away after I receive it?

Yes. Pre-approval is conditional and can be rescinded if the home appraisal comes in below the purchase price or if your financial situation changes before closing.

Recommended

- Pre-Qualification vs. Pre-Approval – Ramy G Girgis – Your Hardest Working Starter-Home Realtor® in Meadow Woods, FL

- knowledge – Ramy G Girgis – Your Hardest Working Starter-Home Realtor® in Meadow Woods, FL

- Your Credit Score and Mortgage Eligibility – Ramy G Girgis – Your Hardest Working Starter-Home Realtor® in Meadow Woods, FL